What is The “Fed Rate” and Why Does It Matter?

First-time Homebuyer Series

When the Federal Reserve makes changes to interest rates, it doesn’t just affect Wall Street—it impacts Main Street, too. The “Fed rate,” or federal funds rate, is the interest rate at which banks lend money to each other overnight. While it’s not the same as mortgage rates, it strongly influences them. When the Fed lowers rates, borrowing becomes cheaper across the economy, including for mortgages, auto loans, and credit cards. For first-time homebuyers, these changes can have an immediate effect on affordability and competition in the housing market.

Affordability Gains

One of the most direct benefits of a Fed rate drop is improved affordability. Mortgage rates are closely tied to the Fed’s policy decisions, so when rates decrease, borrowing becomes less expensive. For first-time buyers, even a small reduction in rates can translate into a meaningful difference in monthly payments.

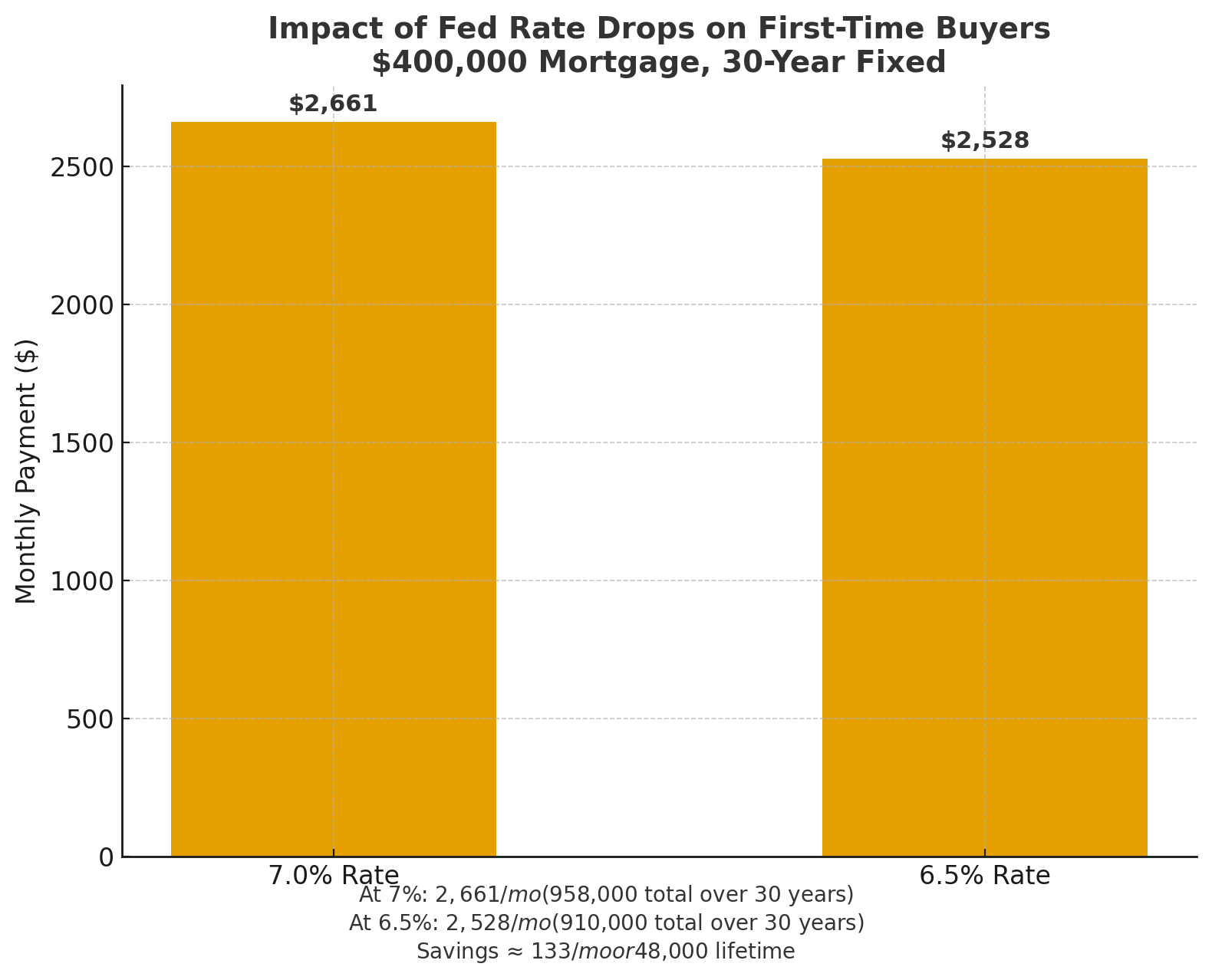

For example, consider a $400,000 mortgage on a 30-year fixed loan:

At 7% interest, the monthly principal and interest payment is about $2,661.

At 6.5% interest, the monthly payment drops to about $2,528.

That’s a savings of roughly $133 per month, or nearly $48,000 over the life of the loan. For many first-time buyers, that difference can mean the ability to afford a larger home, qualify for financing more easily, or simply enjoy more breathing room in their monthly budget.

For renters who have been hesitant about taking the leap into homeownership, rate drops often create the window of opportunity they’ve been waiting for.

Increased Competition

However, lower rates don’t just benefit first-time buyers—they also entice more people into the market. As affordability improves, demand rises. When more buyers are competing for the same limited supply of homes, competition heats up.

This can lead to bidding wars, especially for entry-level homes where inventory is already tight. While lower rates may increase purchasing power, they can also drive prices higher in competitive markets. For first-time buyers, that means preparation is key: getting pre-approved, having a clear budget, and being ready to act quickly can make the difference between winning and losing in a multiple-offer situation.

Balancing the Opportunity

For first-time buyers, the effect of a Fed rate drop is both positive and challenging. On one hand, homes become more affordable on a monthly basis, opening doors that may have previously been out of reach. On the other, increased competition can put pressure on buyers to act fast and sometimes pay more than anticipated.

The key is to approach the market strategically. Work with a knowledgeable agent, understand your true budget, and focus on homes that not only fit your finances but also your long-term goals. Taking advantage of lower rates without overextending yourself will ensure that your first home purchase is both affordable and sustainable.

Bottom Line

Fed rate drops can be a game changer for first-time buyers by lowering the cost of borrowing and expanding affordability. At the same time, they often bring more buyers into the market, creating new challenges in the form of heightened competition. By being prepared, realistic, and strategic, first-time homebuyers can use rate drops to their advantage and step confidently into homeownership.